March 26, 2026

In 2025, DC Byte’s Global Data Centre Index Report as identified APAC as the fastest growing region globally, with a CAGR rate that surpassed EMEA and even the Americas. But almost a year on, what’s changed in APAC?

To answer that question, DC Byte’s analysts look at five key stories from the first quarter of 2026 and what they mean for the region’s data centre ecosystem.

Singapore Renews It’s Role as APAC’s Anchor

Despite ongoing scrutiny around constraints such as land, power and the DC-CFA2 regulation, Singapore still has a role to play as a key anchor for high-value workloads.

In March 2026, Bridge Data Centres said it plans to invest S$3 billion to S$5 billion in Singapore’s next-generation digital infrastructure, with a heavy emphasis on AI-oriented power and cooling systems. At the same time, the company said it is also expanding into Japan, Australia, and the Middle East, underscoring Singapore’s role as both an operating base and a regional command centre.

Why This Matters

This runs counter to the recent industry narrative that Singapore has become too constrained to remain the region’s anchor market. This announcement suggests a more nuanced reality. Singapore is still where operators want to place high-value control functions, advanced infrastructure design, and AI-linked ecosystem investment, even if some bulk capacity continues to spill into nearby markets such as Johor, Batam and Riau.

Chinese Hyperscale Demand is Emerging

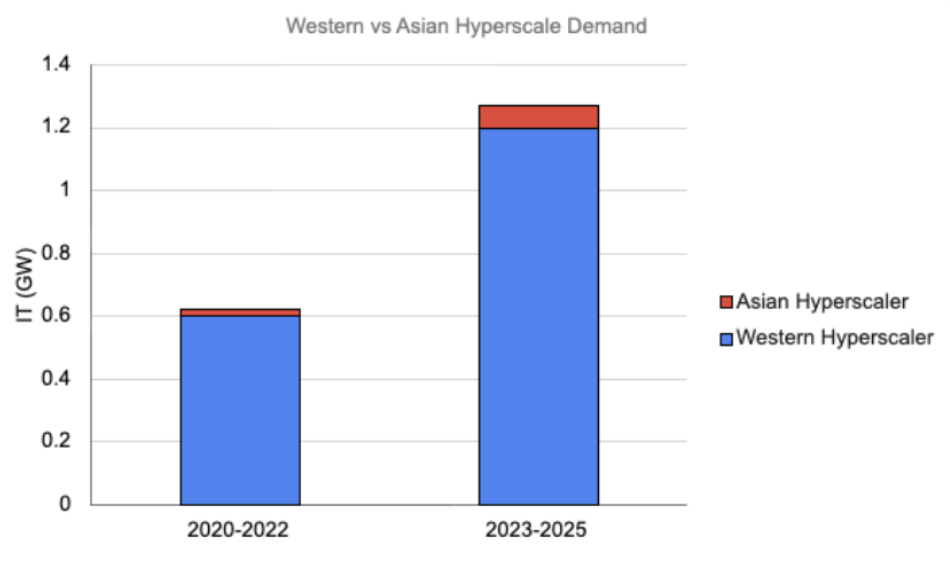

Hyperscale demand within APAC has long been dominated by Western (for which read mostly US) hyperscalers. However, an interesting trend has begun to emerge.

Although, Asian hyperscaler demand remains a fraction of Western (see above) it is expanding. And, notably, at a far quicker rate than Western hyperscalers which is showing signs of slowing. This demand is primarily being driven by Chinese hyperscalers. Chinese demand grew 2.5x from 2020-22 in 2023-25. This compares to a 1x multiple increase from Western hyperscalers.

Although, Asian hyperscaler demand remains a fraction of Western (see above) it is expanding. And, notably, at a far quicker rate than Western hyperscalers which is showing signs of slowing. This demand is primarily being driven by Chinese hyperscalers. Chinese demand grew 2.5x from 2020-22 in 2023-25. This compares to a 1x multiple increase from Western hyperscalers.

Why This Matters

We’re still a long way from a Chinese-dominated market. This growth represents the early stages of development as Chinese hyperscalers begin to look beyond the county’s huge domestic market. However, this is a development to watch closely in the coming years.

Investors Find a Way in Seoul

Delivery conditions in Seoul have been getting tougher for some time now. The Seoul metropolitan area is heavily supply-constrained, due to land and grid limitations. Meanwhile, South Korea’s government has introduced new regulations such as the Power System Impact Assessment, limiting large-scale (>10MW) projects and slowing approval processes, to reduce strain and push development towards regional markets like Busan and Gangwon.

However, some investors are finding ways around the constraints. Earlier in March, Macquarie Asset Management and Gabia announced a strategic partnership to build a next generation hyperscale data centre platform in Seoul, with connectivity support from carrier-neutral operator (and Gabia subsidiary)KINX.

Why This Matters

This partnership, which combines infrastructure capital, cloud and IT services, and carrier-neutral connectivity is exactly the kind of structure operators need to avoid the perils of constrained markets. It could point towards platform formation (where multiple players contribute different strengths to a project) becoming the preferred way to crack difficult markets.

Japan Remains an Important Hyperscale Hub

Japan produced one of the year’s biggest stories yet, when hyperscaler AirTrunk,, secured a JP¥191.6 billion green loan to support the refinancing and continued development of its TOK1 hyperscale data centre campus in East Tokyo. This represents the largest data centre financing ever completed in Japan.

Why This Matters

This loan, hot on the heels of the recent announcement of OSK2, the company’s second Osaka hyperscale data centre, underscores Japan’s role as one of the region’s hyperscale hubs. Alongside this, the announcement signals the growing importance of sustainability‑linked financing to data centre projects.

Johor Is Moving Beyond Its Role as ‘A Singapore Spillover’

Like Indonesia, Malaysian state Johor is has seen two key stories that signal its status as a ‘spillover market’ for Singapore is beginning to change.

First, the announcement in January that TM Nxera (Telekom Malaysia and Singtel’s Nxera) has secured 280MW of power for a new AI-ready campus in Iskandar Puteri. Then, in March, ZData announced a RM8 billion hyperscale project in Gelang Patah, which will become Malaysia’s first GreenRE Platinum-certified data centre.

Why This Matters

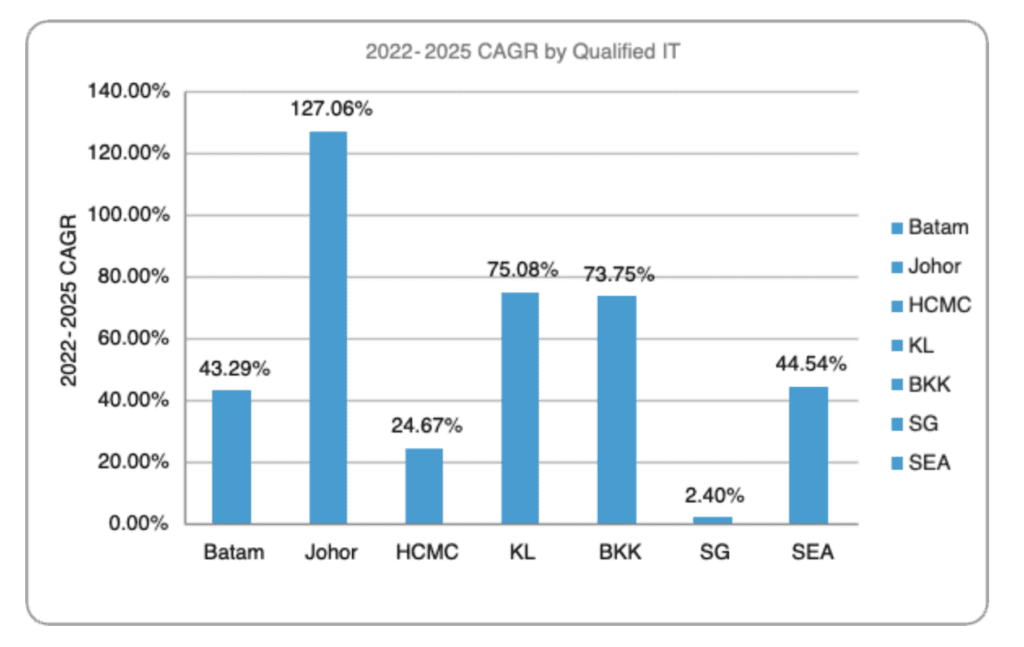

Johor was already one of the world’s fastest growing data centre markets. Indeed, it’s five-year CAGR stands at 127.06%, according to DC Byte data. But until now this growth has largely been driven by spillover demand from Singapore due to its land, power, and regulatory constraints.

However, the announcement of projects like Iskandar Puteri and Gelang Patah could point to a new phase in Johor’s development. Johor is one of the few global markets building multi-gigawatt ecosystems comparable to Northern Virginia-style clusters. Should this continue, the state could become a leading market for hyperscale expansion in its own right.

What Can These Stories Tell Us?

Together, these stories point to an APAC data centre landscape that is becoming more distributed and competitive.

Singapore continues to anchor high value and AI-driven workloads despite ongoing constraints, underscoring its enduring strategic role. Alongside this, Chinese hyperscalers are beginning to influence regional demand as they look beyond their domestic market, an early but important shift to watch.

In more mature markets like Seoul, innovative partnerships are proving essential to navigating land and power limitations, showing how operators can still unlock opportunity in constrained environments. Meanwhile, Johor is emerging as future heavyweight, backed by largescale, AI-ready campuses and increasingly sophisticated financing models that signal their rise into the region’s top tier.

For more on the dynamics shaping APAC’s data centre ecosystem download our latest Market Spotlights and Infographics:

If your planning depends on separating announced capacity from deliverable capacity, you need better visibility on data centre markets, not bigger bets. Book a demo with our team to explore our Market Analytics, where we capture global data centre capacity by market and development stage.

")

")

(1)")