March 18, 2026

North American data center growth continues to dominate industry news. But beyond the headlines, there’s something else happening in the North American ecosystem.

Revisiting key markets in Virginia, Georgia, Pennsylvania and Canada, DC Byte’s analysts have identified an ecosystem that’s decentralizing, concentrating into smaller hubs, and reaching maturity faster than expected. Here’s what that means for growth across the region.

A Strategic Shift for Stakeholders

For operators and developers, the differentiator is increasingly the ability to move from intent to execution. Not because demand is uncertain; development pathways, geography and pipeline maturity now shape how reliably planned capacity is delivered.

For senior decision-makers, this shifts the basis of strategy. Operators and developers need a clearer line of sight on where execution risk is rising and where delivery pathways remain workable. Investors need to price markets by conversion risk, not headline expansion. Suppliers and service providers need to follow where activity is moving, not where it used to be concentrated, and align coverage to the buyer models and submarkets that will convert.

The following changes across Virginia, Georgia, Pennsylvania and Canada serve as practical case studies for how growth reshapes markets under similar conditions:

- Mature hubs decentralize, creating meaningful differences in delivery conditions within a single “core” market.

- Fast-growth states transition into well-established markets, where scale changes competitive dynamics and repeatability become differentiators.

- National markets concentrate into a small number of hubs, while a large share of pipeline sits early in the lifecycle, increasing the importance of upstream visibility and timing.

Virginia

NoVa is still the anchor for Virginia’s data center market. What has changed is the operating model inside the anchor. For example, Loudoun County removed by-right development in 2024. That is a direct shift in how easily incremental capacity can move through the historical core.

The market response is a redistribution of development effort. Divergence in data center development across counties within the state highlight have resulted in fault lines between the market within Loudoun and the ecosystem outside the county. Multiple counties beyond the core are now relevant to tracking and engagement.

Dominion’s contracted load nearly doubled in just five months, making delivery timelines and county-level development pathways a bigger determinant of which projects progress fastest. At that pace, uncertainty in entitlement and sequencing becomes a material cost. The practical advantage shifts toward sites and counties with clearer pathways to execution.

Virginia’s key structural signal is the emergence of a major market with meaningful internal segmentation between hubs. Treating the state as a single, homogeneous hub obscures where delivery pathways remain relatively straightforward and where conditions have materially shifted.

For stakeholders allocating capital, resourcing delivery, or prioritizing commercial coverage, the question becomes which parts of Virginia align with the execution model and risk tolerance required to deliver on schedule.

Read our Virginia Market Spotlight for the full analysis.

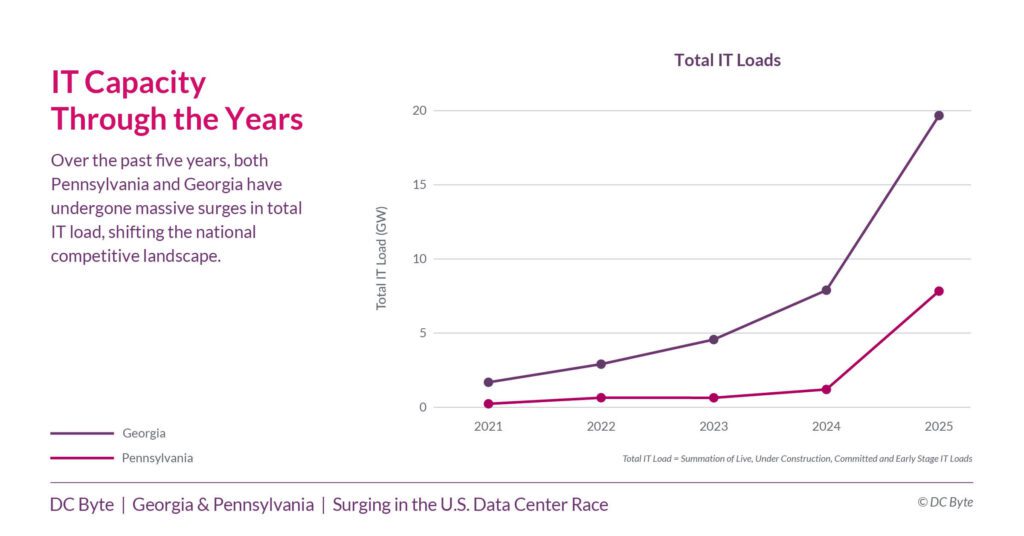

Georgia

Georgia’s trajectory is not incremental. Total IT load has risen rapidly over the past four years, exceeding a 10x increase. At that magnitude, Georgia stops behaving like a high-growth challenger market and starts behaving like a leading market.

Established markets force different strategic discipline. At smaller scale, growth can mask inconsistency because the market is still forming. On a larger scale, inconsistency becomes a drag. The winners are typically those who can execute predictably across multiple sites and cycles, not those optimized for one-off wins. Georgia’s growth numbers imply that the market has moved into that phase.

Georgia’s second order effect is a shift in competitive dynamics driven by scale. The market now supports sustained supplier coverage and competition, with multiple routes to volume across hyperscalers and colocation operators. Stakeholders that align early to the right buyer segments and delivery requirements will be better positioned as the ecosystem matures.

Pennsylvania

Pennsylvania has expanded rapidly from a small 2021 base to a sizable present-day footprint. Rather than a single market, Philadelphia and Pittsburgh are thought of as distinct hubs of development.

This matters because growth expressed across multiple centers tends to fragment the execution landscape. The counterparties, commercial routes and development patterns in one hub are not automatically transferable to the other. A state-level view can capture overall scale, but it can blur where decisions are made and where delivery conditions differ.

Treating Philadelphia and Pittsburgh as distinct hubs enables clearer prioritization and more accurate planning across siting, partnerships and coverage.

Pennsylvania also illustrates a broader point about how North American expansion is unfolding. Growth outside the largest hubs often shows up as a set of clusters scaling in parallel, rather than a single new mega hub. The state’s structure provides a clean example of that cluster-led pattern.

Download our Georgia and Pennsylvania Market Spotlight

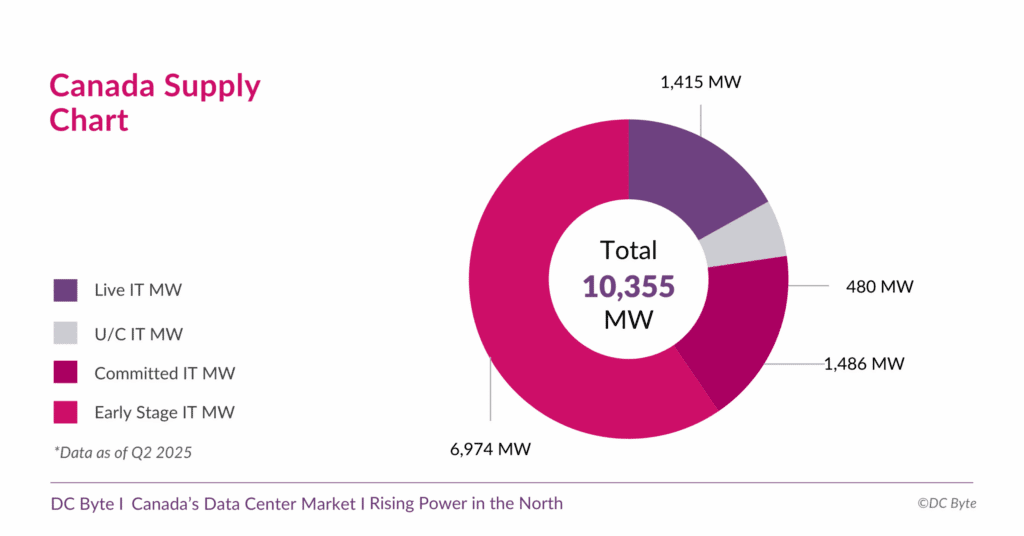

Canada

Canada’s market structure is defined by concentration. Toronto, Montreal and Alberta represent the majority of total IT load, which simplifies prioritization. A small set of hubs captures most of the addressable opportunity, making national coverage and long-term partnership focus more targeted than in more dispersed markets.

Pipeline composition adds the more strategic layer with more than 75% of Canada’s supply sitting in the committed and early-stage categories. That signals forward momentum, but it also signals that timing and progression matter. In an early-weighted pipeline, the capacity story is shaped upstream, where projects are still moving through the stages that determine whether and when they reach delivery.

Canada also carries a grid attribute that can be relevant for enterprise and capital decision-making. Roughly 60% of electricity generation is from hydropower. This provides a measurable energy mix context that some stakeholders will factor into siting, investment, and partnership decisions alongside market scale.

How Market Structure Shapes Delivery

North America’s next phase of data center growth will be shaped by market mechanics rather than headlines. As these spotlights show, outcomes are starting to diverge even where the growth narrative looks similar on paper.

Virginia’s internal segmentation is becoming operationally decisive. Georgia’s scale is pulling the market into a more competitive, repeatability-driven phase. Pennsylvania’s expansion is splintering into distinct hubs rather than a single state market. Meanwhile, Canada’s opportunity remains concentrated, with pipeline weighted early.

The common thread is straightforward. When capacity is scaling at this pace, the differences that matter sit in delivery pathways, submarket structure, and where projects sit in the lifecycle. Those factors increasingly determine which markets convert momentum into delivered capacity, and which ones accumulate friction.

If your planning depends on separating announced capacity from deliverable capacity, you need better visibility on data centre markets, not bigger bets. Book a demo with our team to explore our Market Analytics, where we capture global data centre capacity by market and development stage.

")

")

(1)")