July 16, 2026

For much of the past decade, the debate around hyperscale infrastructure has been framed as a choice. Will the world’s largest technology companies continue building their own data centres, or will they increasingly lease capacity from colocation operators?

It is an understandable question. Hyperscaler demand has become an increasingly important part of the colocation market, while operators are announcing campuses at a scale that would once have been associated almost exclusively with owner-occupied developments. As AI adds further pressure to secure power and capacity, leasing can appear to offer hyperscalers a simpler route to expansion.

Yet DC Byte data suggests that framing the issue as a contest between two strategies misses what is really happening. Colocation is undoubtedly becoming more important. However, self-build still has a crucial role to play. Rather than a choice between the two, the future of hyperscale infrastructure is more likely to be hybrid, with owned and leased facilities coexisting across increasingly complex global portfolios. .

Copyright@DCByte

The Market Is Already Divided

At the end of 2025, approximately one-third of the live capacity used by ten leading hyperscalers was located in colocation facilities rather than hyperscaler-owned data centres.

That overall figure conceals a pronounced divide. AWS, Microsoft, Google, and Meta still own the majority of the capacity they operate. Microsoft has the largest colocation share of the four, at around 40%, followed by AWS at approximately 30%. Google and Meta remain more heavily weighted towards self-build, with colocation accounting for around 20% and 12% of their respective footprints.

The smaller hyperscalers in the analysis follow a very different model. Oracle, ByteDance, Alibaba, CoreWeave, and Tencent operate at or close to 100% colocation, while IBM is also colocation-led.

In other words, hyperscalers are not collectively moving towards a single infrastructure model. The largest companies continue to combine substantial self-built estates with leased capacity, while smaller players depend much more heavily on third-party operators.

This distinction is partly a consequence of scale. The largest hyperscalers have the capital, internal expertise, and long-term demand visibility required to develop their own campuses. Their footprints are large enough to justify direct investment in land, power infrastructure, and construction.

Smaller hyperscalers may have equally ambitious growth plans, but not necessarily the same need, or ability, to reproduce that development model across multiple countries and regions. For them, colocation provides access to established infrastructure without requiring the creation of an equivalent global development platform. The result is not a market migrating from ownership to leasing. It is a market supporting two distinct, but increasingly interconnected, approaches to growth.

Colocation Is Growing Without Displacing Self-Build

The expansion of colocation within hyperscale portfolios is nevertheless significant. Over the past eight years, colocation’s share of hyperscale capacity has nearly doubled, rising from around one-sixth of total capacity to approximately one-third. Growth has continued across every two-year period covered by the analysis, although the pace has moderated slightly in the most recent period.

On the surface, that would appear to support the argument that hyperscalers are progressively abandoning self-build.

The behaviour of individual companies tells a more nuanced story. Not one of the hyperscalers analysed has crossed the 50% threshold during the eight-year period. The four companies that were predominantly self-build remain predominantly self-build, while the hyperscalers that depended on colocation continue to do so.

The largest technology companies are certainly leasing more capacity. AWS, Microsoft, and Google have all increased their use of colocation as their global footprints have expanded. However, they have done so alongside continued investment in their own facilities. Colocation is therefore being added to self-build, rather than replacing it

That matters because it changes how the industry should interpret the growth of hyperscaler leasing. A large colocation agreement is not necessarily evidence of a wider retreat from ownership. It may instead reflect the requirements of a specific market, workload, development timetable, or expansion phase.

The strategic question is increasingly not whether a hyperscaler prefers to own or lease capacity in principle. It is which approach makes the most sense in a particular location and at a particular point in its growth.

Speed Does Not Settle the Argument

One commonly cited advantage of colocation is speed to market. An operator with land, power, planning approval, and construction already under way should, in theory, be able to deliver capacity more quickly than a hyperscaler developing its own site.

The evidence does not show a consistent advantage.

Both colocation and self-build projects take approximately five and a half quarters, on average, to move from construction to live operation. There are differences within individual markets, but the direction varies, and a small number of unusually fast or slow projects can distort the local picture.

However, neither model is therefore systematically faster. This does not mean colocation offers no advantage in entering new markets. An operator that already controls land, power, and permits can still remove several early obstacles from a hyperscaler’s path. However, once construction begins, the delivery timetable appears broadly similar.

The choice between the two models is more likely to depend on a wider set of trade-offs. Self-build can provide greater control over design, operations, and long-term capacity. Colocation can offer capital flexibility, access to established local infrastructure, and a route into markets where power or suitable land is difficult to secure directly.

Neither set of advantages applies equally everywhere. A hyperscaler may prefer to own a large strategic campus in one market while leasing capacity from several operators in another.

Hybrid infrastructure is therefore not simply a compromise between two alternatives. It is a way of matching the delivery model to the commercial and physical conditions of each market.

The Pipeline Points to Further Rebalancing

The forward-looking data suggests that colocation will continue to gain ground.

Approximately 44% of committed and under-construction hyperscale capacity is colocation, compared with around 34% of live capacity. As those projects become operational, leased facilities should account for a larger proportion of the overall hyperscale footprint.

Even here, however, the trend is not uniform.

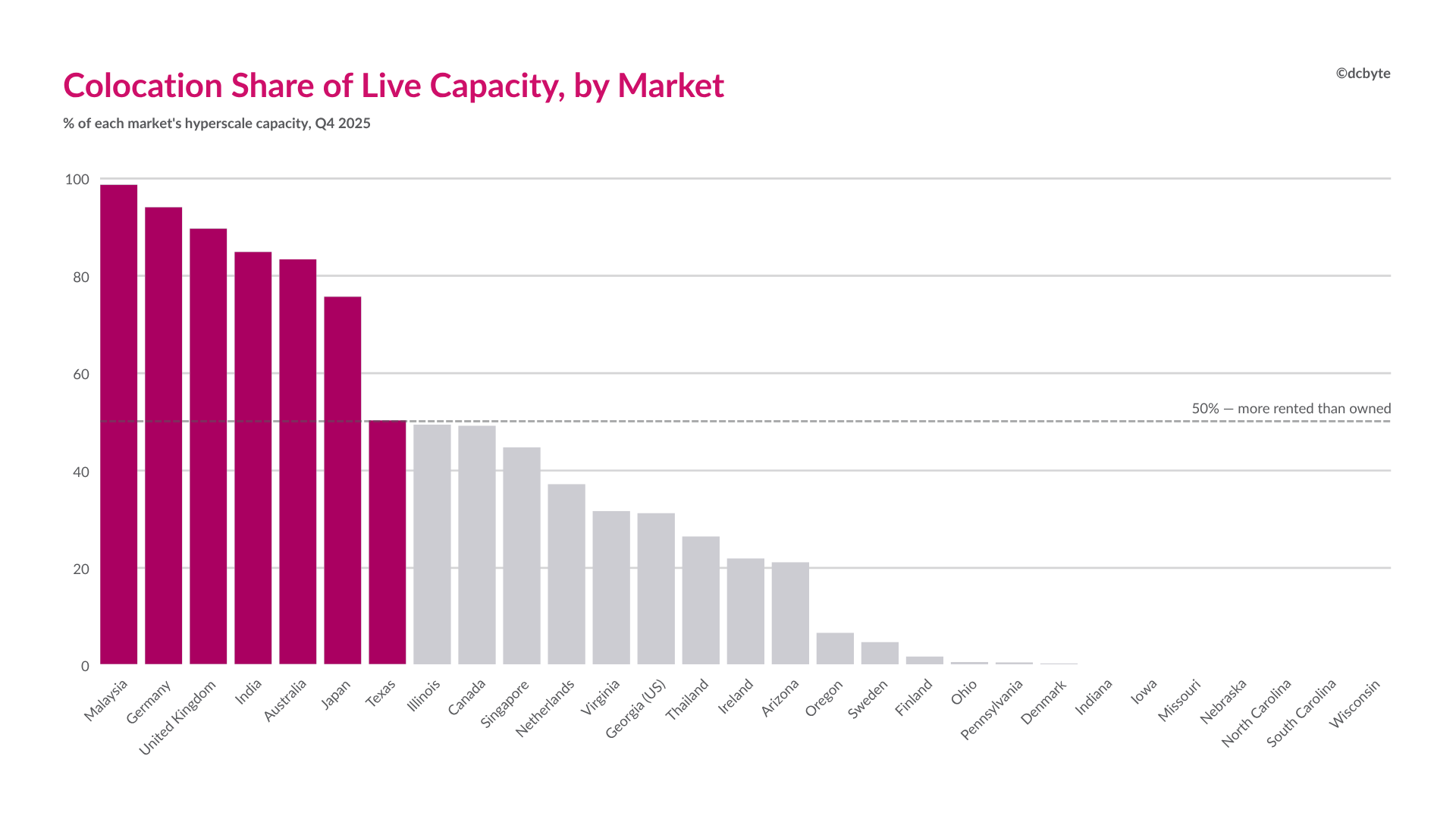

Some markets that have historically been weighted towards self-build are adding more colocation. At the same time, several established colocation hubs, including Malaysia, the UK, India, and Australia, are seeing a greater self-build component within their pipelines.

Copyright@DCByte

Until recently, the largest hyperscale markets tended to be the most heavily weighted towards self-build. By late 2025, that relationship had begun to change, with major markets increasingly leaning towards colocation.

The direction of travel is therefore towards convergence. Self-build markets are adopting more colocation, while some colocation-heavy markets are attracting more owner-occupied development.

This is what a hybrid market looks like in practice. It does not require every hyperscaler or every location to reach a 50:50 split. Instead, both strategies become established parts of the industry’s development model, with the balance changing according to local circumstances.

Hybrid Growth Will Reshape the Supplier Landscape

For colocation operators, the continued growth of leased hyperscale capacity represents a substantial opportunity. The volume of colocation capacity already committed or under construction is around twice the amount currently operating for known hyperscaler customers.

However, operators should not interpret this as a general outsourcing wave in which hyperscalers gradually hand over their entire infrastructure requirements. The opportunity is more selective. Operators will need to demonstrate that they can secure the right combination of power, land, location, and delivery capability in the markets where hyperscalers need capacity. The companies serving the next phase of demand may not be the same businesses that dominated the previous one.

For investors, suppliers, and advisers, the same principle applies. Following hyperscale growth will require more than tracking the total amount of capacity under development. It will require understanding whether that growth is self-built or leased, which operators are involved, and how the balance differs between markets.

The distinction between the two models will also become less useful when assessing the wider supply chain. Both self-build and colocation are expanding. Equipment manufacturers, contractors, power providers, and professional services firms will increasingly need to understand how the two strategies interact rather than treating them as separate markets.

The Best of Both Worlds

Colocation’s growing role in hyperscale infrastructure is clear. Its share of live capacity has nearly doubled in eight years, and its share of the development pipeline is larger still.

But self-build is not disappearing. The world’s largest hyperscalers continue to invest heavily in their own facilities, even as they lease more capacity from third-party operators. Smaller hyperscalers remain overwhelmingly reliant on colocation. At market level, some regions are moving towards leasing while others are seeing renewed self-build activity.

The industry is not progressing towards a point at which one strategy is preferred. It is moving towards a more flexible system in which hyperscalers use both.

The more useful questions are now where each model will be deployed, which operators can support the next phase of leased growth, and how the balance will shift as power and development conditions change.

DC Byte’s Trends in Hyperscaler Build Strategies report examines these questions across ten leading hyperscalers, drawing on eight years of live-capacity data and the committed and under-construction pipeline.

Download the full report to explore how hyperscale build strategies are changing, which markets are absorbing the next wave of capacity, and which colocation operators are positioned to deliver it.

If your planning depends on separating announced capacity from deliverable capacity, you need better visibility on data center markets, not bigger bets. Book a demo with our team to explore our Market Analytics, where we capture global data centre capacity by market and development stage.

Related Posts

")

")

")

")

(1)")

BOOK A DEMO

Discover the Global Data Center Landscape

Join industry leaders using DC Byte to track infrastructure across 135+ countries.