May 18, 2026

Once a market on Europe’s periphery, Finland has emerged as a key location for scalable and sustainable digital infrastructure in the past few years. The Nordic country possesses key advantages ranging from ready access to power to its geographic location, making it of increasing interest to hyperscalers and major operators.

These factors have propelled Finland to its position as the second-fastest growing European market, with a Total IT Load CAGR of over 70% between 2020 and 2025. But what’s behind this growth and is it sustainable? To answer those questions, DC Byte’s analysts look at the reasons behind the market’s rise, potential obstacles to growth, and the future outlook.

Copyright@DCByte

What Makes Finland so Attractive to Operators?

There are several key factors that have proved crucial to Finland’s growth in the past five years.

A surfeit of available brownfield sites: Finland has some real advantages when it comes to land. The country has many conversion-ready brownfield sites, especially in n municipalities like Kajaani, Kemi, and Mantsala. Access to these sites removes many of the zoning and permitting delays that affect other comparable markets.

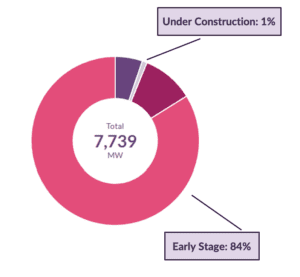

In addition, Finnish state-owned energy company, Fortum, has taken an active role in marketing brownfield sites to specifically attract operators. And this approach is working. Microsoft, Nscale, and DayOne have all committed to projects within the market in recent years, and the country has thousands of MWs in its pipeline. Some 84% of Finland’s capacity is in early stage, with a further 1% under construction, illustrating the scale of demand.

Copyright@DCByte

Waste heat reuse potential: Closely related to the volume of brownfield land, Finland also has huge potential as a waste heat reuse leader. The country has become the largest district heat producer in the Nordics, due to several successful experiments in transforming industrial waste heat from recomissioned pulp and paper sites into clean energy.

Most notable is Google’s Hamina campus, but others include atNorth’s FIN04, the LUMI supercomputer in Kajaanim, and Novagen’s Voikkaa data centre.

These sites demonstrate Finland’s potential for sustainability-conscious operators and hyperscalers looking to build out projects that use energy smartly.

Cheap and easily allocated power deployments: Perhaps Finland’s greatest advantage is the ready access to power it offers data centre projects. Aside from Northern Norway, Finland’s uniform price zone offers the cheapest base prices in the Nordics. The country also possesses strong energy infrastructure, with power historically transported north-to-south along high voltage lines.

Alongside this, Fingrid (the country’s grid operator) is largely accommodating of data centre projects, often prioritising grid connections for operators and offering positive usage guarantees. Finland’s power mix is also one of the cleanest in Europe, with 95% drawn from CO2-free sources, providing an easy way for operators and developers meet ESG targets.

Geographic advantages: Finland is also situated advantageously for operator interest. The country is both close to and possesses good connectivity with mainland Europe and the Nordics, via land and subsea cables. Geopolitical concerns stemming from its proximity to Russia are overshadowed by its membership of the EU and NATO, reputation of its stable democracy, and welcoming business culture.

Copyright@DCByte

Finland’s Global Appeal

Among the Nordic nations, Finland is particularly notable in its attractiveness to international operators. As illustrated above, a much greater diversity of operators are entering the Finnish market with planned hyperscale schemes than anywhere else in the region.

Sweden and Denmark, while attractive to international operators, are both saturated with US hyperscaler demand, making it difficult for new market entrants. Norway does offer similar diversity, but hasn’t typically accommodated demand from APAC, particularly from Chinese cloud and AI operators. As a result, Finland is unique in the region both for its embrace of projects originating from APAC and the diversity of its operator demand.

We’ve covered Finland’s geographic advantages earlier; however, its location is particularly important to international operators. For US hyperscalers, its position in Northern Europe and membership of NATO and the EU, provide it with a reputation as a safe and predictable market to do business. Whereas for eastern hyperscalers its location makes it attractive as a bridge between Northern Europe and Russia, with Asia beyond that.

Obstacles to Growth

Despite its enticements for operators from around the globe, the Finnish market isn’t obstacle free. In fact, there a few developments that any operator or hyperscaler considering the market should watch.

Electricity tax incentive removal: Although there isn’t yet a timeline for the legislation to come into effect, the Finnish government is currently considering a bill to remove the electricity tax incentive for data centres. The proposal would see tax on data centres skyrocket by some 45 times its current rate, removing Finland’s pricing edge over its neighbours.

This is significant because Finland’s comparatively cheap power is undoubtedly its strongest selling point, particularly to hyperscalers and AI projects. While excellent, the country’s connectivity and access to renewable energy isn’t materially better than its near neighbours. Sweden is an instructive example here. Following initial heavy investment from Microsoft and AWS, Sweden repealed its own tax incentives, leading to a plateau in growth in the years since.

Permitting challenges: While Finland’s permitting system is less likely to lead to project delays than other more constrained European markets, the process isn’t always smooth. Unlike Norway and Sweden, power delivery is contingent on receiving building permits from the courts.

This process can take up to three years, depending on the timing of the application (Finnish courts only grant permits at certain times of the year). While far from insurmountable, this challenge can lead to delays, impacting its attractiveness to certainty-hungry hyperscalers.

A potential power crunch: Another potential obstacle for the Finnish market is its reliance on the C-Lion1 subsea cable, connecting the state with Germany. Responsible for 650 MW of power, the 1,200km link is vulnerable to external shocks, whether geopolitical or weather-related. This was illustrated in November 2024, when the cable was severed in mysterious circumstances, leading to a short-term power crunch. The cable has since been repaired. Nevertheless, the incident does demonstrate just how vulnerable the Finnish market can be to external factors.

A note of caution on early–stage developments: Finally, it’s important to note, as we mentioned earlier, that a huge proportion (84%) of Finland’s pipeline is in early stage. This isn’t an ‘obstacle’ per se, but these projects’ development is contingent on a stable, consistent evolution of the market. Any one of the factors above, could create uncertainty, making the market less attractive, particularly to major operators and hyperscalers.

What Does the Future Hold?

International operators’ interest in Finland is well established, and that isn’t likely to change in the immediate future. The country possesses a wealth of infrastructure advantages for data centre development and is well-suited to host the next generation of AI projects. For an illustration of this, all you need do is look at the huge number of projects from international operators in Finland’s pipeline.

However, despite a very promising prognosis for the future, it is worth adding a caveat. All of this is heavily dependent on both the policy decisions made by the Finnish state in the coming years and whether the market can continue to move early-stage projects through its pipeline smoothly. It’s a fine balance, but one that can be tipped in Finland’s favour by making the right decisions now.

If your planning depends on separating announced capacity from deliverable capacity, you need better visibility on data centre markets, not bigger bets. Book a demo with our team to explore our Market Analytics, where we capture global data centre capacity by market and development stage.

Related Posts

")

")

")

")

(1)")

BOOK A DEMO

Discover the Global Data Center Landscape

Join industry leaders using DC Byte to track infrastructure across 135+ countries.