June 4, 2026

The EMEA data centre market has evolved rapidly in the last twelve months. AI-driven demand, power constraints and shifting customer priorities are pushing the industry beyond traditional hubs and forcing new, flexible approaches to design, delivery and financing.

These were just some of the key talking points at DC Byte’s recent EMEA Data Centre Market: Q1 2026 webinar. Scott Roots, EMEA Sales Director, and Kristina Lesnjak, EMEA Research Manager, were joined by industry experts Jochem Steman, Founder of DataLogix, and Warren Barrie, Chief Revenue Officer at Start Campus, to discuss what’s shaping the market in 2026. Here are some of the key takeaways.

The Market Is Expanding Beyond FLAP-D

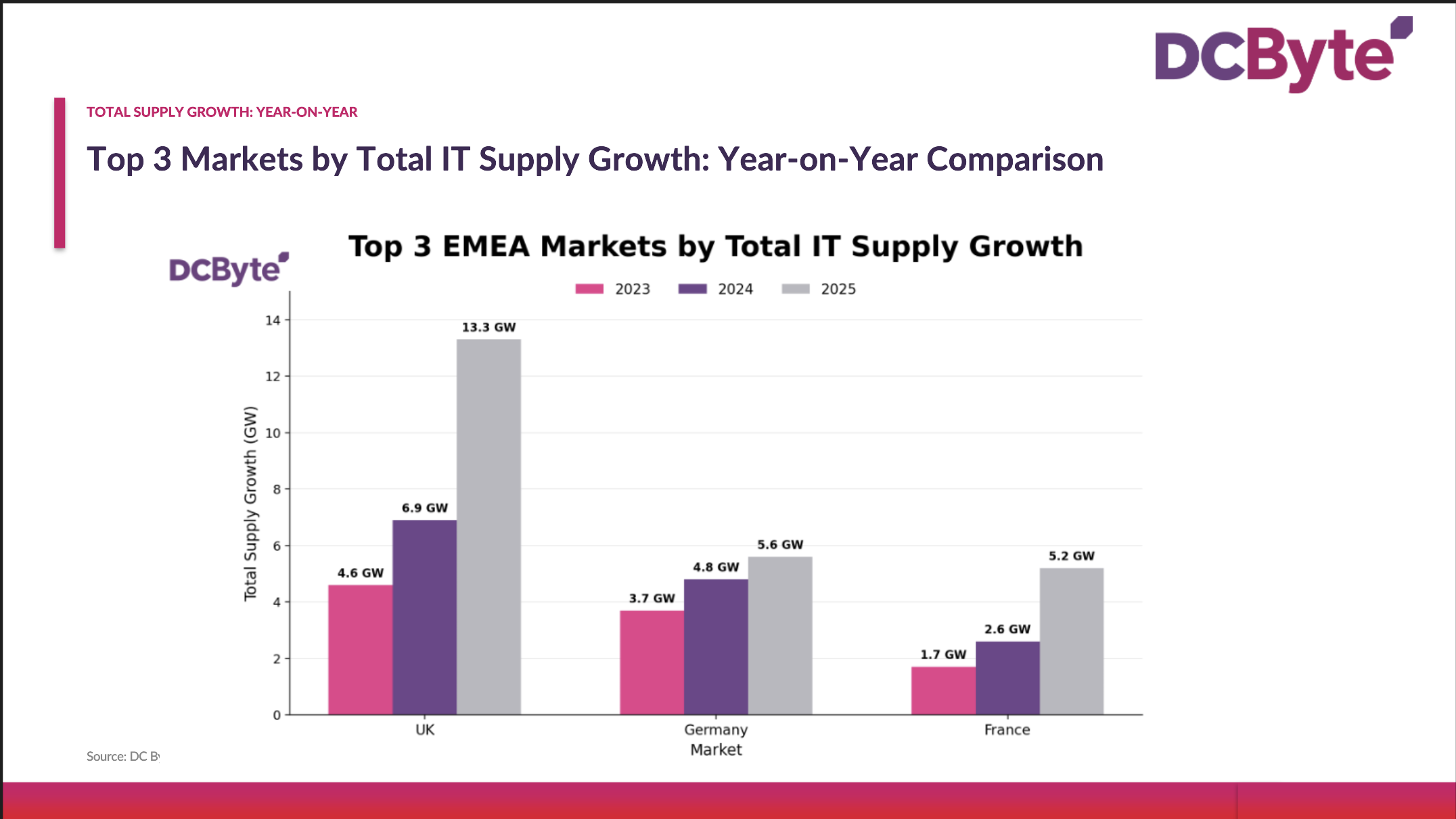

A key theme of the discussion was slowing growth in traditional core markets. London, Frankfurt, Amsterdam and Paris remain important centres, particularly for finance and enterprise demand, but aren’t growing at the rate they once were due to constraints on land and power. The major beneficiaries of this shift have been emerging markets, such as the Nordics, Southern Europe and the Middle East, as Scott Roots explained,

“Pipeline across major markets has slowed down a little, if we consider FLAP-D as the primary markets for EMEA. But we’ve obviously seen a big rise in secondary markets across both Europe and the Middle East.”

However, our panel agreed that not all announced capacity is equal. Similarly to our US webinar, our experts felt that, with AI fuelling headline-grabbing announcements, there’s a clear need to distinguish early-stage intent from deliverable projects.

AI Is Redefining Demand and Location Strategy

AI is now the single biggest driver of new data centre demand across EMEA, according to DC Byte’s Kristina Lesnjak, “Almost every week we see a new gigawatt campus popping up, and there’s a strong push towards secondary markets as FLAP-D becomes more constrained. AI demand is creating a very interesting picture; whereas previously capacity used to be concentrated with established players in established markets, we’re seeing it deployed in places we’ve not seen before.

In the last twelve months, we’ve seen 10–15 GW of developments added to the overall pipeline in EMEA. Of course, the top three markets are still London, Frankfurt and Paris; France, in particular, has really emerged in the last 12 months in terms of the size and scale of the developments we’ve seen there. However, we’re also seeing huge growth in Southern Europe and Iberia, obviously Zaragoza, but in Portugal as well.”

Crucially, AI workloads are also changing how operators and developers think about geography. Training workloads can be highly location-flexible, while inference still requires proximity to users and networks. As Warren Barrie explained, “If the workload is very aligned to training models, operators can be location agnostic, which is why we’re seeing expansion into unusual secondary markets. In contrast, if the workload is inference, then clearly metros with access to consumers become critically important.” The key implication is that workload type, rather than a market’s reputation, is increasingly driving site selection in EMEA.

Speed is Everything for Hyperscalers and Neo-clouds

Across hyperscalers, neo-clouds and AI platforms, speed has overtaken almost every other consideration. As Warren put it, “Among our customers, who are primarily hyperscalers and neo-clouds building at scale, the single biggest driver is time to market. How quickly can you stand capacity up, and is your supply chain and operational setup mature enough to handle large scale?”

Warren went on to explain that speed to market is closely followed by scale and long-term runway, with energy economics completing the picture, “If I had to rank it, I’d say time to market, then scale combined with runway, then renewables and access to low-cost energy.” The message from our panellists was clear: those operators with proven delivery capability and ready-to-scale campuses are best placed to meet AI and hyperscaler demand.

This is also driving a push towards brownfield development in secondary markets, according to Kristina. “One thing we’re seeing in emerging markets is that operators are opting to retrofit brownfield sites instead of building from scratch on greenfield land. Especially for neo-clouds that need to deliver capacity fast, brownfield sites offer a ready grid connection and avoid rezoning delays.”

Constraints are Wider than Just Power Availability

While much of the discourse around constraints centres on power availability, our panel felt that many people focus on the wrong issue. Even in power-rich markets, such as the Nordics, transmission and grid access are often the real constraint rather than availability itself.

As Warren explained, power alone does not make a viable market. Fibre connectivity, accessibility and workforce availability are equally critical. “Power is definitely the underpinning ingredient required for all customers. However, access to fibre and accessibility are still important. You can build a site in the northern reaches of the Arctic Circle, but if you can’t get there easily and you can’t connect that facility easily, then you’re presented with further challenges.

For example, the north of Norway has an abundance of power and cheap land, and Iceland has plenty of hydropower. But fundamentally, you need people there to build it, which is difficult in a climate that only allows construction four or five months of the year. An optimal region for development needs subsea cables, an engineering base of thousands, and access to key neighbouring markets. Getting land is one thing, but these factors are equally important.”

Our panel also cited supply chain bottlenecks and labour shortages as further delivery risks to watch. As Warren said, “We’re seeing long lead times for high-voltage equipment, switchgear, and chipsets for end users. In most cases, 24 months is the minimum.”

Jochem went further, stressing the role of skills shortages in lead times, “Some operators are working together with customers to speed things up. Customers will often have their own supply chain and spare stock. However, people are also key. We need a lot of skilled workers just to build a project, so labour availability can be just as constraining.”

Flexibility is Becoming Key to Design

Throughout the sector, facilities are getting larger and densities are rising to cater for AI and hyperscaler demand. As a result, developers and operators are being forced to build with an eye to the future. As Jochem explained, “Current designs need to be flexible. If you’re in the neo-cloud space, you know that you have an early refresh cycle. The best way to do this is through modular systems, where you evolve your data centre as you go to cater for new demands.” This includes planning for greater use of technologies like liquid cooling. As Warren noted, “As chipsets advance, you’re going to see less reliance on air and more reliance on liquid, so operators have to cater for that.”

In a similar vein, energy procurement is also becoming more workload-aware and hybridised. As Warren explained, “We’re increasingly seeing businesses structure power procurement around a real understanding of what their workload profile is like, we’re seeing a real hybrid approach to power procurement.”

Capital Has Become More Selective

Despite the challenges faced by the industry, our panel agreed that investment capital is not in short supply. However, the way capital funds projects is changing, as Jochem elaborated, “AI-focused neo-clouds are entering the market aggressively, often with shorter contract terms. Traditional hyperscaler contracts were ten to fifteen years, whereas neo-cloud contracts are five to seven. This poses problems for financing large-scale builds. For campus-style developments, shorter terms don’t work, especially if you’re investing at the building level. As a result, capital is becoming more selective in what attracts investment and what doesn’t, with longer terms preferred.”

The Bottom Line

Throughout all the topics covered by our panel, one theme was universal: whether for power procurement, choosing sites or accessing investment, flexibility has become key to success in the EMEA data centre ecosystem. This has become particularly important in an era of surging demand and growing constraints across the region. The lesson is clear. The operators, developers and investors who’ll succeed are those who focus on deliverability over raw demand and are able to think laterally about where and how they deploy projects.

Want to hear more from our panel of data centre experts? Watch our EMEA webinar in full here.

If your planning depends on separating announced capacity from deliverable capacity, you need better visibility on data center markets, not bigger bets. Book a demo with our team to explore our Market Analytics, where we capture global data centre capacity by market and development stage.

Related Posts

")

")

")

")

(1)")

BOOK A DEMO

Discover the Global Data Center Landscape

Join industry leaders using DC Byte to track infrastructure across 135+ countries.